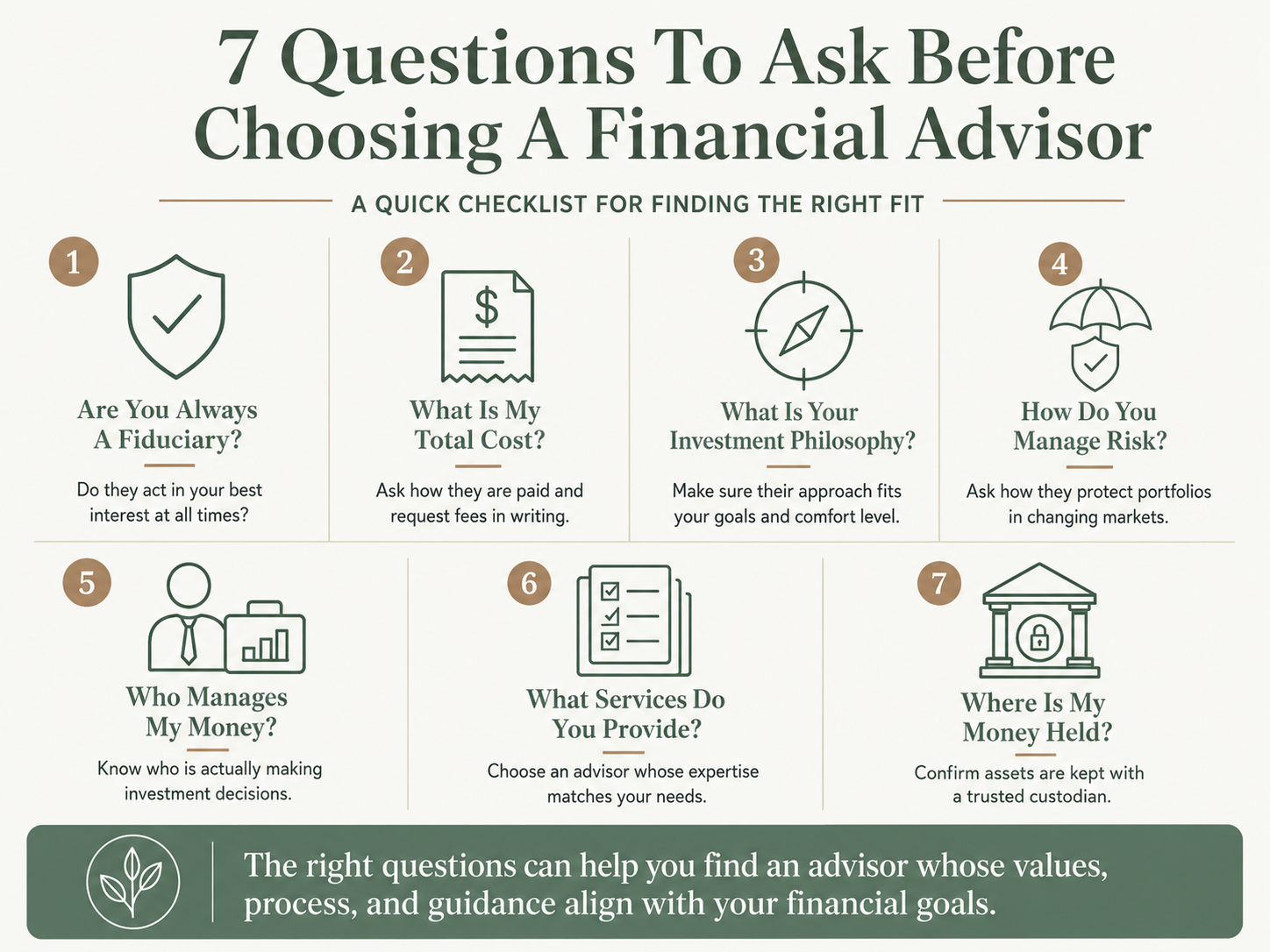

7 Questions to Ask a Financial Advisor

7 Essential Questions to Ask When Choosing a Financial Advisor

Congratulations on taking the first step in either hiring your financial advisor/reevaluating your previous choice of advisor.

Selecting a financial advisor could be considered one of the most impactful decisions you make. Unfortunately, not all advisors are created equal. Asking the right questions to discover values, ethics and philosophy that align with you will avoid potential headaches.

These 7 questions are designed to weed out the unsuitable advisors and identify which advisors deserve to go to the next step with you.

1. Are you a fiduciary all the time?

A fiduciary is someone who acts in the best interest of their clients all the time.

There are no hidden agendas, no products and no goals besides that of the clients.

This essentially means the only source of revenue to the advisor is from you and no one else.

Why is this important to know?

Loyalty will be to whoever compensates the advisor.

Not all advisors are fiduciaries.

Some advisors will be part of a larger company, these advisors can be “dually registered.”

One day they are a fiduciary putting your interests first and the next they are trying to sell you an insurance/investment product with hidden commissions.

No matter what you may think you already know, ask your current/potential advisor if they are a fiduciary and how their flow of compensation is structured. Be sure to include questions about any conflict of interest when it comes with their parent company, many institutional firms are heavily compensated from mutual fund companies just to prioritize their funds.

2. What is my total cost to work with you? How are you compensated? Where can I see this in writing?

Just because you work with a financial advisor who is a fiduciary 100% of the time, doesn’t mean it’s easy to understand the all-in costs.

Here are some of the common fees you might pay when working with a fiduciary financial advisor:

- Advice Fees. These can be in the form of hourly fees, one-time project fees, or a percentage of your investments.

- Transaction Fees. These are charged by the custodian (e.g., Fidelity, Schwab) when your advisor buys or sells investments on your behalf and can range from $0 to $50 per trade.

- Expense Ratio. This fee is charged by a mutual fund or exchange-traded fund (ETF) to cover operational expenses and can range from 0% to 3% (or more!) per year.

It’s important to note that a financial advisor who serves as a fiduciary is only compensated by the advice fee.

While they don’t benefit from other fees, they still have a legal responsibility to keep those costs low.

For example, let’s say your fiduciary advisor recommends that you put $100,000 in the S&P 500.

Here are two S&P 500 mutual funds and their expense ratios (as of 1/25/2023):

- Rydex S&P 500 (RYSOX) = 1.65% or $1,680 per year

- Fidelity S&P 500 (FXAIX) = 0.015% or $15 per year

That’s a difference of $1,665 per year!

When two investments appear to be identical (like the example above), your financial advisor who serves as a fiduciary is obligated to recommend the lower-cost option.

This is why it’s so important to ask about all the fees you might incur.

Every SEC-Registered financial advisor is required to give you their Form ADV and Form CRS. These documents will give you a detailed breakdown of their services and fees.

3. What is your investment philosophy?

Each advisor will have their own unique approach to investing your money. Investing is a complex topic that can be quite overwhelming when learning about a specific style. Rely on your gut to tell you if it fits your own philosophy.

In general, an advisor will be active or passive. Active means they believe they have a strategy that can better accomplish a specific goal than what the market averages. Passive means they believe the market cannot be beaten in any way and prefer to let money sit and ride out the ups and downs.

ASK THIS FOLLOW-UP QUESTION: What else do you do for your fee other than manage my investments?

If they use a passive strategy and don’t offer other specific services, this should be a red flag.

4. What is your portfolio risk management strategy?

Managing risk should be at the core of a financial plan. Years of returns can be washed away with moments of unfortunate events.

No one has a crystal ball on what the markets will do, this doesn’t excuse advisors from having a concrete plan to protect your nest egg.

The industry will say financial advisors need to be passive investors and just take the hits of the market when they come. The phrase you will likely hear is “buy and hold,” it is most accurately represented as an on off switch.

Having an investment philosophy that allows flexibility of your advisor to be flexible in your accounts according to market changes is key. This can be related to adjusting the volume of the tv.

5. Who will manage my money?

Technology has changed how advisors can manage money.

It is all too common for advisors to pawn off the management of investments.

When this happens, the advisor will put your investments in second place behind finding new clients.

You want an advisor who is responsible for your money and can tell you exactly what is happening.

6. What services do you provide? Who do you specialize in working with?

Would you go to a chiropractor for a broken bone? No, you would go to a trained MD to be treated. Similarly, you will not go to a financial advisor just for investment advice if you also need help with retirement planning.

When you ask the advisor what services they provide, figure out how long they’ve been working in that area and ask for some real-life examples.

If your current/potential advisor doesn’t offer what you truly need, look elsewhere. Don’t use a small motor to a large boat.

7. Where do you keep my money and how can I see it?

This question may seem odd, but this is important. The importance of this question comes down to avoiding money schemes, like Bernie Madoff.

The issue with Bernie Madoff is that his clients wrote checks to Bernie directly to invest their money. He then placed the money into his personal bank account! You can see the issue.

The safest and proper way is for you to make the checks out to the custodian of where your money will be invested (Charles Schwab, Fidelity, Vanguard, etc.). Thus, the money never touches the advisor’s hand.

In conclusion, choosing the right financial advisor can have a significant impact on your financial health and overall well-being. Asking the right questions can help you assess whether a potential advisor is a good fit for your needs and goals. By inquiring about their qualifications, compensation structure, investment philosophy, and approach to risk management, you can gain valuable insights into their expertise and suitability. Don't hesitate to ask follow-up questions or seek out multiple opinions before making a decision. With a little due diligence and careful consideration, you can find an advisor who will help you achieve your financial objectives and build a brighter future.

Related Posts: Aligning Your Investment Strategy with Your Financial Goals (4 Minute Read) | What Are Common Investment Mistakes to Avoid?